The Environmental Forces Shaping the Attractions Industry in 2026—And the Opportunities They Bring

When I sit down to write the yearly strategy plan for Gantom, I begin, as most do, with a SWOT and environmental analysis. I review top stories from 2025, industry research, and trend reports to identify the environmental forces shaping the attractions industry.

Those environmental forces inspired this week’s episode of Green Tagged, and also this newsletter.

We wanted to give you both the strategy (how to think about these forces) and the execution (the actual steps you can take). This isn’t a comprehensive industry report. It’s our read on the major currents and some ideas for how to position yourself to ride them rather than get swept away.

Capital Is Moving

The Biggest Bets Are International

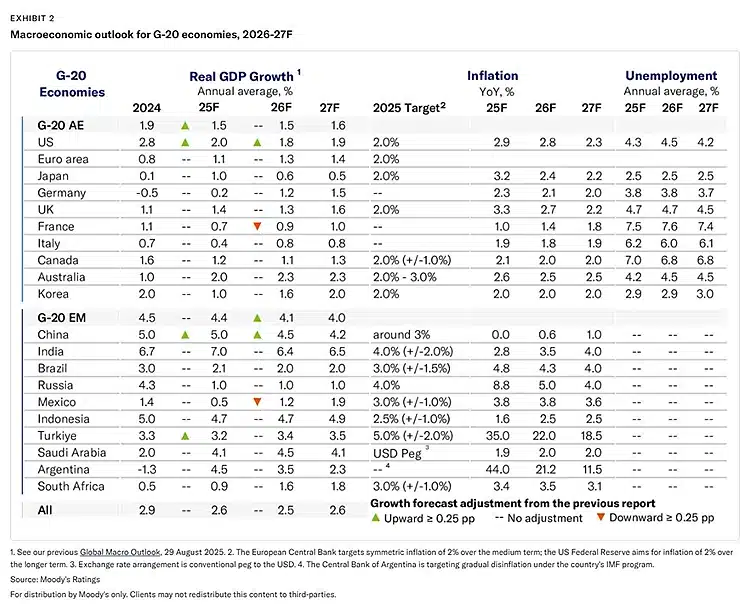

While the U.S. pipeline remains steady, the largest new capital deployments are overwhelmingly international. Moody’s describes the global outlook as “mixed,” with “advanced economies growing modestly and emerging markets mostly maintaining stronger momentum.” That divergence is increasingly reflected in where major operators are placing their biggest bets.

The industry’s most capital-intensive projects sit outside the U.S.: Universal’s planned UK resort, Disney’s development in Abu Dhabi, large-scale destination builds in Saudi Arabia, Merlin’s Harry Potter expansion at LEGOLAND Germany, and Japan’s first permanent Pokémon theme park. These projects align with Moody’s expectation that emerging markets will grow at a rate closer to 4.0% annually, far outpacing advanced economies.

Global growth is expected to “hover around 2.5% in 2026 and 2027,” but that average masks wide regional differences. Capital is not disappearing—it is being redeployed toward markets with stronger long-term demand and government-backed development frameworks.

What We’re Watching (2026-2031)

This is a selected list of highlights we’re tracking, not a comprehensive industry report.

United States:

Dollywood’s NightFlight Expedition — $50M indoor coaster-rafting hybrid, largest investment in park history

Universal Kids Resort, Texas — Seven themed lands, 300-room hotel, opening 2026

Rock ‘n’ Roller Coaster Muppets — First Disney thrill ride featuring the Muppets, 2026

LEGOLAND Galacticoaster — $90M space-themed land at California and Florida parks

Fast & Furious: Hollywood Drift — 70+ mph outdoor coaster at Universal Studios Hollywood

Netflix House Las Vegas — Third location on the Strip, opening 2027

International:

Universal UK — £50B investment, 8.5M projected first-year visitors, opens 2031 in Bedford

Disney Abu Dhabi — Major new park in development

Universal Saudi Arabia — Early planning stages, Qiddiya destination

Harry Potter at LEGOLAND Germany — Merlin’s largest single-site investment ever

Pokémon theme park, Japan — World’s first permanent Pokémon park, opens February 2026

Six Flags Qiddiya City & Aqua Rabia — Already opening in Saudi Arabia

The Opportunity:

U.S. momentum can sustain near-term activity, but your growth will be limited if you rely solely on domestic projects. That means:

Ensuring your supply chain can support international projects

Building relationships with international operators now, before you need them

Understanding regulatory differences across markets

Investing in team members with international experience

The Great Fragmentation: Time Versus Money

Guest expectations aren’t just changing—they’re splitting into two distinct camps. Call it the K-shaped economy. Call it a generational shift. Whatever the cause, the effect is clear: design and pricing are being pushed toward opposite ends of the spectrum.

The Value-Minded Guest wants a full evening’s entertainment without nickel-and-diming. They’re exhausted from a full work week and won’t tolerate overcrowding, endless lines, or planning fatigue. They’ll pay—but they want it packaged as all-inclusive.

The VIP-Minded Guest has money but no time. They expect zero waiting and a premium experience. They won’t blink at price tags that would make the value guest faint.

Scott put it perfectly in our episode: “You may have to target either five $1 million tickets or $1 million of $5 tickets. You may not be able to be both.”

The Opportunity: Understand where your audience sits on this spectrum and reduce friction for them specifically.

For value-minded audiences, this doesn’t mean losing revenue—it means restructuring how you present pricing. Bundle your offerings. Make the sticker price feel honest and complete. Remove the surprise upcharges that erode trust.

For VIP audiences, invest in premium experiences, even if you sell only a handful. Halloween Horror Nights’ private tours, Disney’s guided VIP experiences, Horror Unleashed’s premium packages—these pay for themselves with just a few sales. Design for the VIP experience because the economics work even at low volume.

Creature Comforts Are Non-Negotiable

Here’s what guests won’t tolerate anymore: planning for necessities.

They expect quality food worth the price. Not carnival fare with restaurant prices, but actual good food they’d want to eat outside the park. Bad food is no longer just disappointing—it actively devalues the entire experience.

They expect sufficient, clean restrooms. They expect good merchandise. They expect shelter from the weather. These aren’t nice-to-haves. They’re table stakes.

Guests are also beginning to expect more premium experiences – Six Flags’ Conjuring experience proved this—guests showed they’ll pay premium prices for haunted attractions when the quality justifies the cost. The value equation isn’t about cheap versus expensive; it’s about fair value for what’s delivered.

The Opportunity: Audit your basic offerings with fresh eyes. Ask yourself:

Would I eat this food at these prices if I weren’t at my attraction?

Are restroom facilities sufficient for peak capacity, and are they maintained?

Does my merchandise reflect what guests want to remember about their visit?

If the weather turns bad, do guests have adequate shelter that maintains the experience?

Attractions with poor facilities signal poor value, regardless of how good the rides are. Fix the basics first.

The Museum Renaissance

According to the TEA Global Attendance Report, museums are having a moment. The reasons make sense: they’re indoors (protected from increasingly unpredictable weather), prices are typically all-inclusive (eliminating the planning fatigue we discussed), and they’re experimenting with IP in ways that feel fresh. The Franklin Institute, premiering “UNIVERSAL THEME PARKS: THE EXHIBITION” this year, shows how museums are borrowing from theme park playbooks while theme parks borrow their IPs.

Museums offer what outdoor attractions increasingly struggle to guarantee: a predictable, comfortable experience where the ticket price covers everything.

The Opportunity: Weather is becoming less predictable, not more. How are you planning for it?

This isn’t about building a museum. It’s about asking whether your attraction has adequate indoor components for when the weather goes sideways. Can guests still have a meaningful experience if it’s 105°F or pouring rain? Do you have contingency programming that maintains value when outdoor attractions close?

The parks that thrive in 2026 and beyond will be those that don’t ask guests to gamble on weather.

Trust Is Dead, Authenticity Matters More

- User-generated content drives action: Oregon parks with highly-engaged geotagged posts saw 4-4.2% monthly increases in visitation. The kicker? Only authentic, user-generated content had this effect—professional productions showed zero impact.

- Raw content generates 8.7× more engagement than branded content, according to AdWeek. As industry expert Dan Fleyshman puts it: “There will be 500-800% more engagement from a mobile phone than a fancy camera.”

- Entertainment and interactivity matter most: A 2024 study of 412 Gen Z/Millennial travelers found that entertainment value and user engagement (likes, comments, shares) drove behavioral intentions—not production quality or information density.

- Show, don’t tell. Raw guest footage and user-generated content should be a staple of your strategy

- Less polish, more personality. Behind-the-scenes content, staff personalities, real moments shot on phones

- In-person experiences become more valuable. When digital reality is suspect, physical experiences that guests can touch, feel, and verify become premium

The Era of Uncertainty Remains

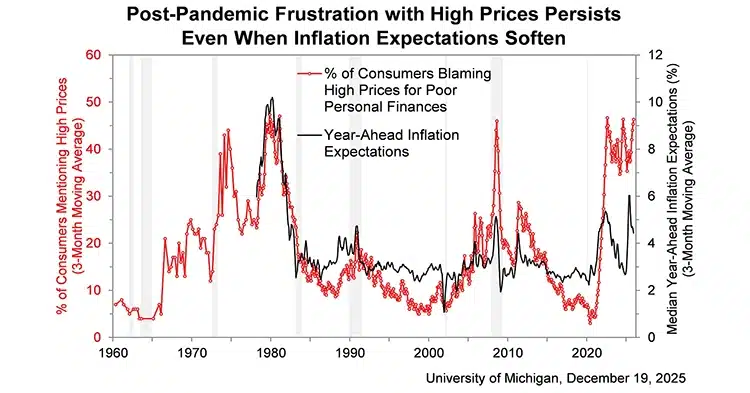

Trade policy uncertainty has spiked to near-record levels—higher even than during COVID—according to the Economic Policy Uncertainty Index. Consumer sentiment has plunged 28.5% year-over-year, with the University of Michigan’s Index of Consumer Sentiment falling from 74.0 in December 2024 to 52.9 in December 2025. Nearly half of consumers (46%) blame high prices for their poor personal finances—a level not seen since the early 1980s.

Tariffs remain unpredictable. Immigration policy shifts weekly. International tourism patterns are volatile. Political instability continues.

It’s a mess out there.

The Opportunity: We’ve done this before. We survived a pandemic that shut down the entire industry. The playbook hasn’t changed—it’s intensified.

Diversification is your hedge. Ask yourself:

If that new coaster costs 30% more due to tariffs, what’s your backup plan?

If international tourists can’t reach you, how do you make up that revenue with locals?

If your primary demographic gets squeezed economically, do you have offerings that appeal to different audience segments?

If your main season gets hit by unprecedented weather, do you have indoor alternatives or shoulder-season events?

Scenario planning isn’t pessimism—it’s a survival strategy. The attractions that thrive won’t be those that predicted the future correctly; they’ll be those that built flexibility to adapt to multiple futures.

Action items for 2026:

Evaluate your international readiness. Even if you’re not working internationally today, could you if the opportunity arose?

Know your audience position. Are you serving value-minded guests, VIP guests, or trying to do both? Stop hedging and commit.

Audit your basics. Food, restrooms, weather contingencies. Fix what’s broken before investing in the next big attraction.

Rethink your content strategy. Less production value, more authenticity. Show real people having real experiences.

Build scenario plans. What’s your backup if costs increase 30%? If international tourism drops? If your primary season sees unprecedented weather?

The attractions industry has survived worse than uncertainty. We’ll survive 2026 too. But survival isn’t the goal—opportunity is. And in times of upheaval, the prepared don’t just survive. They thrive.